While Parliamentarians run berserk inside the holy citadel of democracy on the issue of price inflation and the common man is forced to live with the dual terror of price rise and bandhs, it could well be worth our while to ruminate over the nature of inflation in general as well as the form it has assumed in India in particular.

While Parliamentarians run berserk inside the holy citadel of democracy on the issue of price inflation and the common man is forced to live with the dual terror of price rise and bandhs, it could well be worth our while to ruminate over the nature of inflation in general as well as the form it has assumed in India in particular.

As far as generalities go, let us note at the very outset that even if the rate of inflation remains constant, prices will continue to increase. Thus, if the rate of inflation were to be 2 per cent per year forever, then a commodity that costs Rupees 100 today, will be sold at Rs. 102 a year from now and then at Rs. 104.04 the year following and so on.

A corollary of this observation is that a fall in the rate of inflation does not imply a fall in prices. To illustrate once again, suppose that the rate of inflation were 2 per cent during the current year and then it falls to 1 per cent during the subsequent year. In this case, one would pay Rs. 102 a year onwards for a commodity he purchases for Rs. 100 today. However, two years down the line, the price would be Rs. 103.02 instead of Rs. 104.04 as in the first example. In other words, a fall in the rate of inflation would still entail a rise in prices, though the rate at which prices rise over time would be lower. If, on the other hand, the rate rises from 2 to 3 per cent, then two years from now the price would be Rs. 105.06. An increasing rate of inflation, unfortunately, is what afflicts India. And, as our charts demonstrate below, this is not a recent phenomenon.

Assurances from the Government, therefore, regarding an expected arrest in the rise in the rate of inflation means precious little for the poor man. If the rate of inflation falls but remains positive, the intensity of his struggle for survival can only increase, since the prices would be higher than what he paid prior to the fall itself. In concrete terms, even if the rate of inflation falls to 5 per cent by December, 2010, prices on an average will be higher than they are today.

Going over now to particulars, what does the Indian variety of inflation look like? To start with, we need to inquire if inflation is a recent phenomenon at all. The period 2001-02 to 2009-10 will suffice to answer the question.

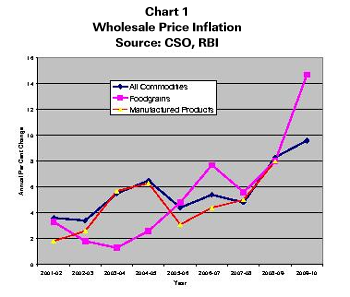

Chart 1 reveals the behaviour of annual rates of inflation of wholesale prices. Prices of three different items, "all commodities", "foodgrains" and "manufactured products" have been chosen for the purpose. Despite occasional dips in the annual rates of inflation, the trend is clearly positive for all three groups. Hence, wholesale prices have been rising since 2001 at least and, by and large, they have risen at a rising rate. The other interesting feature that emerges from the chart is that beyond 2003-04, foodgrain prices rose the most.

Chart 1 reveals the behaviour of annual rates of inflation of wholesale prices. Prices of three different items, "all commodities", "foodgrains" and "manufactured products" have been chosen for the purpose. Despite occasional dips in the annual rates of inflation, the trend is clearly positive for all three groups. Hence, wholesale prices have been rising since 2001 at least and, by and large, they have risen at a rising rate. The other interesting feature that emerges from the chart is that beyond 2003-04, foodgrain prices rose the most.

Why have foodgrains been more vulnerable to the inflation virus?

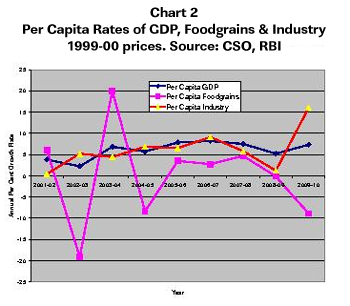

Chart 2 provides a simple explanation. It shows that the per capita output of foodgrain in India has been erratic to say the least. Further, its annual rate of growth exceeded that of the per capita GDP and industrial output only in 2001-02 and 2003-04. During all other years, it has been well below and, worse, its rates of growth were actually negative during 2002-03, 2004-05 and 2009-10. In fact, the underlying data reveals that in 2008-09 too, the rate of growth of foodgrain output was marginally negative (- 0.2 per cent). In other words, per capita foodgrain output has been generally on the decline in India over a long period of time, though the recent failure of monsoon has made matters worse. What is well-known now is that it has displayed a downward trend since the year 1990.

Chart 2 provides a simple explanation. It shows that the per capita output of foodgrain in India has been erratic to say the least. Further, its annual rate of growth exceeded that of the per capita GDP and industrial output only in 2001-02 and 2003-04. During all other years, it has been well below and, worse, its rates of growth were actually negative during 2002-03, 2004-05 and 2009-10. In fact, the underlying data reveals that in 2008-09 too, the rate of growth of foodgrain output was marginally negative (- 0.2 per cent). In other words, per capita foodgrain output has been generally on the decline in India over a long period of time, though the recent failure of monsoon has made matters worse. What is well-known now is that it has displayed a downward trend since the year 1990.

Compared to this situation, per capita growth rates of both the GDP as well as the industrial output have been relatively steady and increasing at annual rates within the 5-10 per cent band. Under the circumstances it is clear that agricultural prices must rise faster than industrial prices, as Chart 1 reveals. In economic jargon, the agriculture-industry terms of trade has been moving in favour of agriculture, a situation that is reminiscent of the pre-green revolution days.

Our first chart captures the behaviour of wholesale prices only. In the real world though, it is the retail price that matters ultimately for the common man and this is captured by the consumer price indices.

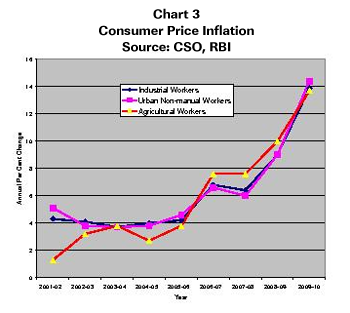

Chart 3 shows the behaviour of three of these retail price indices, the "industrial workers' price index", the "urban non-manual workers' price index" and the "agricultural workers' price index". These indices are constructed by taking into account the pattern of expenditure incurred in the market by the corresponding social classes.

Chart 3 shows the behaviour of three of these retail price indices, the "industrial workers' price index", the "urban non-manual workers' price index" and the "agricultural workers' price index". These indices are constructed by taking into account the pattern of expenditure incurred in the market by the corresponding social classes.

The chart is alarming.

While all three price indices appear to display similar trends of annual rates of inflation, the agricultural workers' price inflation has been consistently higher from 2005-06 or so till almost the end of the period under consideration. Taking into account the fact that the poorest members of India's population are agricultural workers, it is clear enough that rural India is the worst victim of inflation.

To emphasize the point, during the year 2006-07, India's per capita real GDP and the agricultural workers' price index grew simultaneously at the rates of 8.2 per cent and 7.6 per cent respectively. The latter in turn was higher than the growth in both the other price indices. It is strange indeed that our politicians have woken up to the problem so recently, the history of the problem being older than what many appear to believe.

Any discussion on inflation remains incomplete without reference to the petro price debate. The Parikh Committee has recommended the linking of petro prices to markets. Its arguments have their merits, since distorting prices away from markets distorts resource allocation. However, the Government has implemented the recommendation partially, especially by sticking to the wedge between petrol and diesel prices. Technologically speaking, the production costs of diesel and petrol are no different from each other. Nonetheless, on account of the better road mileage offered by diesel, it is still being subsidized in the interest of the transport sector. This makes some sense of course in view of the inflation story we have told. However, the sense disappears when diesel is used to run generators in multi-storied buildings, in multiplexes and so on during power cuts. The automobile industry is turning out large number of diesel operated, air-conditioned passenger cars. The sensible approach would be to charge those who can afford to pay the same price for diesel and petrol. The extra revenue so obtained can be used to subsidize the mass transport of commodities as well as of people.

A similar argument applies to the pricing of LPG cylinders purchased by 5 Star hotels, expensive restaurants as well as middle class families and the wealthy. As pointed out earlier, inflation is not a temporary phenomenon. It has probably come to stay, but policies such as these would go a long way towards making our growth dreams inclusive rather than exclusive.